Does “having a life” mean you have to spend every single cent you make? It can feel that way, with the cost of nice restaurants, trendy cafes and hipster pop-ups adding up very quickly.

But that doesn’t have to be the case. You don’t have to choose between enjoying yourself and saving money – these sensible ideas will help you find the compromise that works for your lifestyle.

Set an eating-out budget

Who says you can’t go out or do what you want while you’re trying to save money? Consider the maximum amount you’d like to spend on eating out per month – then divide it by the number of weeks.

For example, you might want to spend $500 a month of your income on eating out, which works out to $125 per week. And think about your habits: while some people spend more on eating and drinking with friends after work, others spend more on weekends when work isn’t in the way.

Also take note of holidays, which can derail your plans if you don’t take those days into account. The cost of all that merrymaking can add up.

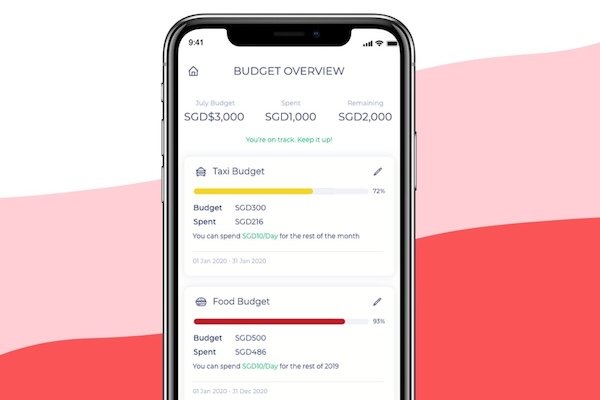

Good news is, we’ve made your budgeting effortless with the budget function in the Planner Bee app, free for all users.

Be reasonable and constantly review

It doesn’t make sense to set an unrealistically low budget that you can’t stick to. There’s no need to cause yourself grief, or decide that you have to be a hermit because you’ve busted a tiny budget.

You might need time and experimentation to figure out a sum that works for you, so consistent reviewing of your budget each week will help you make better choices the following week. You’ll also feel more in control of your savings progress, and not dread being locked into spending only an unfeasibly small figure for too long.

Look for deals

Sometimes it’s difficult thinking of new places to go to with friends. So instead of searching for new cafe openings, why not try searching for new promos to check out instead? You’ll get to discover new places, and get discounts, too.

There are apps, food blogs, and credit cards providing discounts for parties of two or more, so it’s a great excuse to meet up with people and enjoy a deal together.

Pack your lunch

If your social life is packed, and you want to go out after work and on weekends, lunch at work might be your least important meal.

Cut back on costs with a packed meal. Meal-prepping for the week allows you to cook and buy in bulk, for better prices, and you get to control your diet at the same time too, leaving more calories for after work. (But that’s probably a tip for another blog.)

Working from home? Know when to treat yourself

Chances are you’ve already spent a lot of time working from home, and that’s probably not going to change any time soon. It’s the perfect chance to save money on meals, and keep enough in reserve to really splurge when the situation calls for it.

If you’d already started packing lunches to work, you can now put together a meal fresh just as you’re getting hungry, or plan home lunches with family members in advance to maximise savings. If you’re heading out to buy something, dishes are probably cheaper in your neighbourhood than in the CBD or city centre.

And while you’ll then have more money on hand to enjoy your weekend in full, don’t be afraid to be kind to yourself and have a treat or two during the week now and then – working from home in isolation can bring a person down.

Automate your savings

Create a standing instruction on your salary crediting account three days after payday. Set the amount you wish to save, and have it transferred to another bank account.

Since this is automatic, it helps keep the money away from you, which can be useful in months where you’re more remiss in your spending. Plus, it’s pretty nice to see the balance in that account steadily going up, and provides a little emergency fund too.

Read more: What’s an Emergency Fund and How Much is Enough?

The same theory could work for investing too. You could set up a regular investment plan, as little as $100/month. It works like a savings account with the potential to grow. Just note that you should not look at it as a short-term investment as there are often charges for each investment. Liquidating soon after, before the money has even started to make profits, will not make any sense.

Read more: Investment Portfolio Basics: What is it, and How to Build One?

Conclusion

It’s all about striking a balance. Give yourself some room to enjoy yourself – just not too much! Set sensible spending and saving targets, hunt down some juicy deals, cut spending in less important areas and focus on what you really enjoy, and you’ll be able to both eat out and feel satisfied looking at your savings steadily growing.

Have more tips and tricks to share? Reach out to us at ask@plannerbee.co!