Navigating health insurance can be intimidating, and many neglect the need to prepare for the unexpectedness of critical illnesses.

When a person is covered by critical illness (CI) insurance, they get financial security in the face of expensive and life-altering medical conditions, as well as added peace of mind while recovering from the illness.

CI insurance plans in Singapore usually cover 37 medical conditions, with some policies offering a wider coverage. Out of these 37, cancer, stroke, and heart attack rank among the most common in Singapore, with cancer accounting for the highest percentage of death in Singapore.

In this article, we delve into the intricacies of CI insurance in Singapore, exploring its significance, coverage options, and considerations for individuals seeking to safeguard their well-being and financial stability against unforeseen health challenges.

Importance of critical illness insurance

It’s a common misconception in Singapore that CI insurance is unnecessary, and many think it’s not needed if they already have basic life insurance policies. Unfortunately, that is not true.

If you are diagnosed with a critical illness such as cancer, a life policy will only pay out in the event of death of permanent disability. Hospitalisation insurance is also not a substitute as it only covers your medical bills.

With CI insurance, you are given a fixed sum should you be diagnosed with an illness covered under the plan. This payout can help you avoid financial issues if you need to stop working or require long-term treatment. You can use the payout for anything such as transportation, living expenses, and utility bills.

Besides a standalone CI plan, you can also get a critical illness rider with your life insurance to receive a fixed sum payout upon diagnosis.

Considerations

Depending on your income, expenses, savings, and number of dependents, everyone’s insurance needs will differ. To understand how much protection you will need for critical illnesses, you can use Planner Bee’s insurance calculator to get an estimate.

Then, you should ask yourself to what extent you would need coverage when it comes to CI. While there are more than the 37 listed critical illnesses, different plans cover slightly different illnesses. Depending on your needs and financial ability, you might only want to be insured against the top three critical illnesses in Singapore: cancer, stroke, and heart attack.

Let’s look at three critical illness insurance plans that cover these top killers and see how they compare against one another.

Tiq’s 3 Plus Critical Illness

Tiq’s 3 Plus Critical Illness insurance is a protection term insurance that provides coverage for all stages of cancer, major heart attacks, and major strokes.

| Factors | Details |

| What it Covers | – Cancer (Early to advanced stages) – Stroke with Permanent Neurological Deficit – Heart Attack of Specified Severity |

| Eligibility | – Singaporean citizen or permanent resident with a valid NRIC or a foreigner holding a valid Work pass/Permit or Long-term Visit pass – Between 17-70 years old (yearly renewable up to age 85) – Residing in Singapore |

| Cover Amount | S$30,000-S$300,000 (in multiples of S$1000) |

| Premiums | Depends on your cover amount and age Payment: Monthly, quarterly, semi-annually, annually |

| Death Benefit | S$20,000 |

| Riders? | (Optional) Heart and Neurological Disorder Rider |

By logging in with Singpass and filling up a simple health declaration survey, you can register for the policy within a few clicks.

For illustration purposes, if you are a 30 year-old man who does not smoke and wants the maximum coverage of S$300,000, your premiums will increase every year based on your age like this:

Accurate as of April 2024

Tiq provides complimentary cover for your children and death benefits of S$20,000 per child for up to four children. The plan also offers special conditions coverage including a 20% payout against Diabetic Complications or Severe Rheumatoid Arthritis (SRA).

Although this post is not influenced or paid for by any sponsors, applying through our affiliate link here will help support our research and content creation.

FWD Big 3 Critical Illness Insurance Coverage

Similar to Tiq, FWD also offers the Big 3 Critical Illness Insurance Coverage to cover cancer, heart attack, and stroke.

| Factors | Details |

| What it Covers | – Cancer (Early to advanced stages) – Major Stage Stroke – Major Stage Heart Attack |

| Eligibility | – Singaporean citizen or permanent resident with a valid NRIC or FIN – Between 17-65 years old (yearly renewable up to age 85) – No existing FWD Cancer Insurance, FWD Heart Attack Insurance, or FWD Stroke Insurance |

| Cover Amount | S$50,000-S$200,000 |

| Premiums | Depends on your cover amount and age Payment: Monthly, annually |

| Death Benefit | S$20,000 |

| Riders? | (Optional) Heart and Neurological Disorder Rider |

If you are a 30 year-old male who does not smoke and wants the maximum coverage of S$200,000, your premiums will increase every year based on your age like this:

Accurate as of April 2024

Compared to Tiq’s 3 Plus Critical Illness, premiums for FWD are approximately half the amount with a maximum cover amount about $100,000 lower.. For example, over 20 years, you would pay a cumulative sum of S$10,110 with FWD versus S$22,641 with Tiq.

Other than that, both plans are very similar in their coverage and payment terms. Deciding between the two boils down to the amount of coverage you want and your budget.

HSBC Term Protector

HSBC’s Term Protector with the Early Critical Illness rider is pretty different from Tiq’s and FWD’s.

| Factors | Details |

| What it Covers | Early to advanced-stage critical illnesses |

| Eligibility | – Singaporean citizen or permanent resident with a valid NRIC or FIN – Between 1 month-70 years old (yearly renewable up to age 99) |

| Total Benefits | S$100,000-S$2,000,000 |

| Premiums | Depends on your cover amount and age Payment: Monthly, quarterly, semi-annually, annually |

| Death Benefit | According to the chosen sum |

| Riders | Early Critical Illness Payout Advance Critical Illness Payout Advance Total and Permanent Disability Payout Disability Cash Benefit Critical Illness Plus Benefit Personal Accident Benefit Guaranteed Survival Payout |

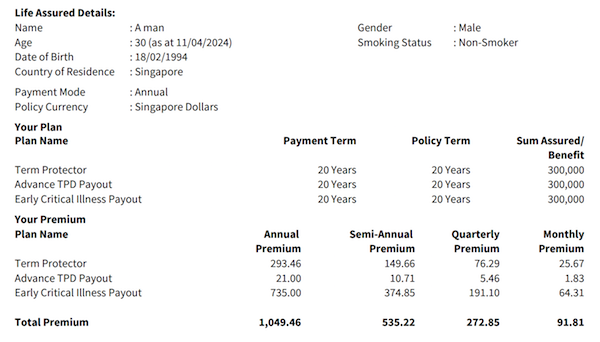

In the HSBC Term Protector case, if you are 30 years old this year looking for S$300,000 in coverage, you will pay fixed premiums of S$1,049 annually. This totals to S$20,980 in 20 years.

Accurate as of April 2024

Compared to Tiq’s CI plan, you will have to pay almost double the price in your first year, but eventually, pay less in premiums towards the end of the payment plan. HSBC’s plan is also approximately S$1,600 cheaper than Tiq’s CI plan over the course of 20 years.

Furthermore, instead of Tiq’s and FWD’s death benefit of S$20,000, HSBC’s plan provides the full S$300,000 death benefit payout as it is a term plan as well.

Comparison at a glance

When buying critical illness insurance, you should look at long-term costs because you never know when unexpected illnesses can hit. A fixed-premium structure would be less costly if you want a long-term insurance plan. Let’s look at the pros and cons of each policy:

| Plan | Tiq 3 Plus Critical Illness | FWD Big 3 Critical Illness Insurance Coverage | HSBC Term Protector with Early Critical Illness Payout |

| Pros | – Complementary cover for up to four children – Able to cancel anytime after two months – Can purchase directly from website | – Affordable premiums – Can purchase directly from website | – Level premiums – Covers more than 37 critical illnesses – High death benefit of S$300,000 |

| Cons | – Stepped premiums – Only covers three critical illnesses | – Stepped premiums – Only covers three critical illnesses | – Minimum of a 5-year plan |

Read more: I Already Have Hospitalisation Insurance. Why Do I Need A Critical Illness Plan Too?

Standalone cancer insurance

Among the three common critical illnesses, cancer is the most prevalent illness amongst Singaporeans — nearly 46 people in Singapore are diagnosed with cancer every day, and it is the leading cause of death.

Some people may only want insurance against cancer based on their budget and preference. Some insurance providers offer standalone cancer insurance which provides a payout in the event of a cancer diagnosis.

Get protected today

In the labyrinth of modern health issues, few hover as ominously as cancer, stroke, and heart attack. These illnesses strike without warning, disrupting and threatening the lives of not just the patient but their families as well.

From adopting healthier habits to being sufficiently protected from critical illnesses, you should start taking proactive steps to bridge any protection gaps you might have to mitigate the impact of these diseases.

If you are unsure which plan best suits you or would like a customised quote, leave your request via this form. Planner Bee will work with you to find the options that best suit your needs.