Cancer treatment is a notoriously hefty expense. Taking the first step to discuss viable insurance plans can go a very long way in protecting you and your family’s finances.

Insurance plans can cover a wide range of unforeseen medical emergencies, from treating minor accidental injuries to long-term medical treatments. In this article, we’ll be deep-diving into one of Singapore’s leading critical illnesses and what you can do to prepare financially.

Prevalence of cancer in Singapore

The Ministry of Health has named cancer the leading cause of death in Singapore, with the number of cancer cases on the rise in recent years.

The Singapore Cancer Society estimates that 46 people are diagnosed with cancer and 16 people in Singapore die of cancer causes every day. It is also projected that 1 in 4 people may develop cancer in their lifetime.

Among women in Singapore, breast, colorectal, and lung cancer are the top-ranked cancers while prostate, colorectal, and lung cancer are among the top-ranked cancers among the country’s male population.

While these figures may be alarming, it is possible to have better clinical outcomes through early detection, treatment, and a critical illness insurance plan to pay for those treatments.

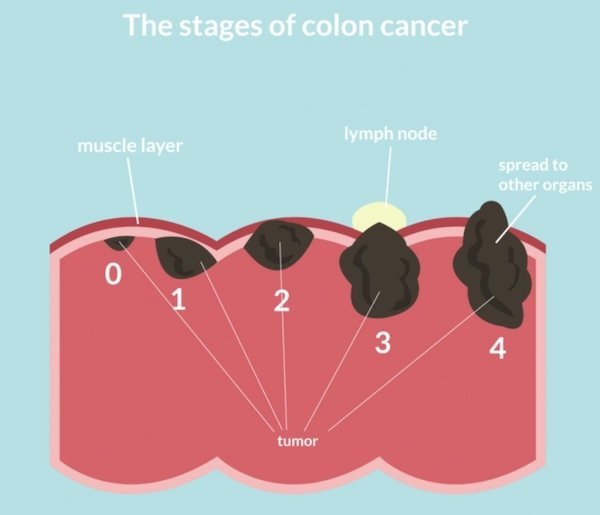

Different stages of cancer

Before we delve further into cancer insurance, we need a better understanding of cancer.

Cancer is typically diagnosed at various stages: Stage 0, Stage 1, Stage 2 or 3, and Stage 4. Depending on the stage, it could affect the type of insurance you need and the payouts involved.

Stage 0 means there are abnormal cancer cells situated in place and have yet to spread from where they started. While this is no cause for alarm just yet, it is helpful to remove the tumour entirely through surgery to prevent cancer from developing any further.

At Stage 1, the cancer is small and contained within the organ of origin, and hasn’t spread into nearby tissues, lymph nodes, or other areas in the body. This is often referred to as early-stage cancer.

In Stages 2 and 3, the cancer is much larger and has spread into nearby tissues or lymph nodes, but has not spread into other parts of the body.

Stage 4 is the most critical phase, where it has spread to other organs and deep tissues in the body and has reached the final stage of development. This can also be referred to as advanced or metastatic cancer.

Depending on the standalone cancer plan or critical illness insurance you have, some insurers only pay out the lump sum at the later stages while others would pay out with an early-stage diagnosis.

Average cost of cancer treatment in Singapore

Cancer is expensive to treat, and it’s no different in Singapore.

The expenditure on cancer drugs is increasing by 20% a year compared to 6% for other drugs. Cancer drugs accounted for one-quarter of total drug spending in Singapore in 2019, at S$375 million, and is projected to reach S$2.7 billion in 2030.

The cost of cancer treatment in Singapore can also place a heavy burden on your finances. While the government’s healthcare schemes help in defraying some of the costs, they cannot cover everything.

Below are some of the estimated inpatient procedure costs related to common cancers in Singapore:

Condition | Public Hospital | Private Hospital | |

| Subsidised | Unsubsidised | ||

| Abdomen, lining, cancer, surgical removal | S$7,489 | S$26,898 | N.A. |

| Cancer of the blood and lymph nodes without very severe complications | S$2,329 | S$8,363 | S$13,710 |

| Breast cancer, malignancy with catastrophic or severe complications | S$2,113 | S$3,707 | S$5,039 |

| Airway, lungs abnormal growth with very severe complications | S$3,194 | S$8,832 | S$28,108 |

| Male reproductive tract, removal of entire prostate and surroundings | S$9,400 | S$27,495 | S$58,355 |

| Cancer of liver, gall bladder, bile duct or pancreas with catastrophic complications | S$3,410 | S$9,970 | S$33,642 |

Source: MOH Hospital Bills and Fee Benchmarks

On top of these costs, there are also other financial burdens such as chemotherapy, cancer drug medication costs, loss of income, transportation costs, and more. With all the expenses added up, a cancer diagnosis might cause a person to use up their life savings.

What is a standalone cancer insurance plan?

In response to the increasing diagnosis and cost of treatment in Singapore, insurers have launched standalone insurance plans to cover cancers from early to advanced stages.

These specialised insurance plans are used to relieve the loss of income from being unable to work due to a cancer diagnosis, as well as the additional costs involved. This could include procedures like breast reconstruction, alternative treatment and medicine, home care services, and additional supplementary costs.

With that said, a major change in coverage for cancer treatment kicked in in April 2023, transforming how private insurers cover cancer treatment costs.

Instead of “as-charged”, Integrated Shield Plans (IPs) from private insurers now come with an upper coverage limit. Additionally, IPs will only cover treatments and drugs on the Cancer Drug List (CDL) for outpatient cancer treatments.

See more: Changes to Medishield Life Coverage for Cancer Treatment and How It Affects Cancer Patients

Medical insurance vs critical illness insurance vs cancer insurance

There is a common misconception that medical insurance and critical illness insurance can be used interchangeably, but they are two very different policies serving different purposes. Critical illness insurance is also very different from standalone cancer insurance.

A medical insurance plan protects you in the event of a medical emergency and covers your medical expenses and hospitalisation costs. Such hospitalisation costs are hard to estimate as it depends on the diagnosis and treatment required.

For instance, the bill for a severe case of stomach flu for a two-day hospitalisation stay would cost a lot less than one for cancer, where treatment may involve operations and chemotherapy sessions. In both these cases, the costs incurred will be covered by medical insurance.

In the case of a critical illness like stroke or cancer, a critical illness insurance plan provides a lump sum payout based on the sum determined at the point where you purchase the insurance. The payout is based on how much you have insured, regardless of the expenditures incurred due to the critical illness.

In Singapore, the Life Insurance Association (LIA) defines the list of critical illnesses covered. As of 2019, there are 37 medical conditions covered under this framework.

Standalone cancer insurance is a type of critical illness plan. It will provide a payout just like a critical illness plan, but only in the event of a cancer diagnosis.

Meanwhile, standalone cancer insurance is a type of critical illness plan. It will provide a payout, just like a critical illness plan, but only in the event of a cancer diagnosis. If a person only has a standalone cancer plan and not a critical illness plan, there will be no payout in the event of a stroke or heart attack.

A standalone cancer plan can also be a useful supplement to one’s critical illness plan. In the case of a cancer diagnosis, you can claim the cancer plan and save the critical illness plan for another severe disease.

As most medical insurance plans reimburse the costs of medical treatment as per the bill, the lump sum payout from a standalone cancer plan or a critical illness plan can help families to better plan care for the patient and cope with the potential loss of income during the treatment period. This sum could also help with medical expenses that medical insurance does not cover including home nursing, transportation, and household expenses.

| Policy Type | What it does |

| Medical Insurance | Covers hospitalisation costs and medical expenses up to a certain amount depending on riders involved. Plan continues as long as premiums are paid |

| Critical Illness Insurance | Lump sum payout if diagnosed with one of the 37 critical illnesses. Plan is terminated upon payout. |

| Cancer Insurance | Lump-sum payout if diagnosed with cancer. Plan is terminated upon payout. |

Manage your insurance policies with Planner Bee

Critical illnesses like cancer must not be taken lightly. While making different lifestyle changes can reduce the risk of cancer or prevent its rapid spread, we should also prioritise financial planning to be prepared for such unforeseen circumstances.

Planner Bee is able to help you manage your insurance policies, savings, and expenses more efficiently. Users can view their categorised and synced insurance policies and receive a personalised overview of their total insurance payables each year with Planner Bee.

If you wish to know more about medical insurance, critical illness insurance, or standalone cancer plans, feel free to contact us at ask@plannerbee.co today!

Read more: All You Need to Know About Critical Illness Insurance in Singapore