A critical illness (CI) diagnosis is mentally and physically challenging for the patient. It is also often financially burdensome for patients and their families. Even when detected early, critical illnesses can still be life-threatening and require extensive and expensive medical treatments.

However, if the patient is adequately protected by their CI insurance, the payout can relieve much of the financial burden, allowing the patient to focus on recovery. This, in turn, can also ease some of the patient’s mental stress, knowing that their family’s financial stability is not at risk.

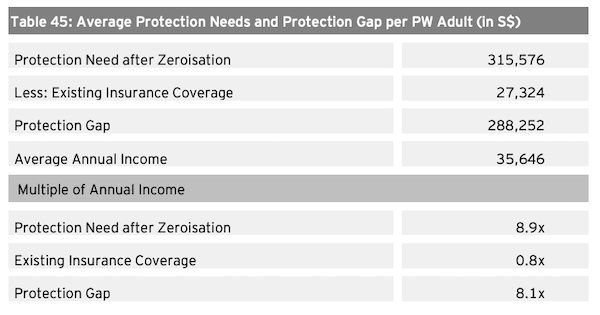

Unfortunately, according to the 2022 Protection Gap Study, the average Singaporean’s CI coverage is 8.1 times less than what is estimated to be needed. That translates to an eye-watering sum of S$288,252.

A stumbling block for many when it comes to CI coverage is often that it is costly. In this piece, we will debunk five of the most common myths about CI insurance.

Credit: 2022 Protection Gap Study

Myth 1: I already have health insurance and do not need CI Insurance

When diagnosed with a CI, your health insurance kicks in to cover your medical expenses. A proper health insurance plan should handle the bulk of your medical expenses, which can include hospitalisation, surgery, and medication costs.

What sets a CI insurance plan apart from other health insurance policies is the way it pays out. A lump sum is payable upon the diagnosis of the CI, as long as it is covered within the plan or rider purchased, instead of merely reimbursement of medical expenses.

Since a CI diagnosis typically requires a longer treatment period, it can cause an extended loss of income. The lump sum payout can help cover other costs such as transportation to and from the hospital, providing financial support for your family if you are the sole breadwinner, and during your recovery period.

Read more: I Already Have Hospitalisation Insurance. Why Do I Need a Critical Illness Plan As Well?

Myth 2: CI Insurance is too expensive

Contrary to popular belief, a CI plan is relatively affordable, especially for young working adults when they are still healthy and free of illnesses.

For instance, FWD’s Big 3 Critical Illness plan covers all stages of cancer, late-stage heart attack, and late-stage stroke, with a premium that averages about S$20 a month for a 30-year-old male and non-smoker. The payout is about S$100,000 should the insured get a related CI diagnosis. The 3 Plus Critical Illness by Tiq has a S$100,000 payout and covers all stages of cancer, heart attack, stroke, diabetic complications, and severe rheumatoid arthritis diagnosis. That only costs S$9.15 a month for a 30-year-old male who is also a non-smoker.

The eCriticalCare by DBS offers comprehensive cover for death and 37 different critical illnesses. However, instead of yearly renewal, this plan offers policy terms of 10 to 40 years, in multiples of five years. For a 30-year-old male who is a non-smoker, a 10-year policy term and coverage of S$100,000 will only cost S$14.61 monthly.

Depending on how early you start your CI protection, it can go as low as S$6 a month for substantial coverage. CI insurance is not as expensive as you think it is.

Myth 3: My family doesn’t have a history of CI, so I don’t need coverage

While some health conditions are genetic, they can still be caused by factors in your environment or your lifestyle. Having a healthy lifestyle and exercising regularly can reduce your risk of CI. But the unexpected can still happen and we are not always in full control of our health.

During the period from 2017-2021, 84,002 cancer cases were reported in Singapore. In 2020 alone, there were 8,846 reported stroke cases in Singapore. Additionally, according to the Singapore Myocardial Infarction Registry Report 2020, there were 11,631 heart attack cases in Singapore. That is an average of 31 a day.

Having a CI plan can help put your mind at ease should something unexpected happen, providing a significant lump sum payout to cover any loss of income. Furthermore, they start at a low price for most young adults and should be something you can consider getting for peace of mind.

Myth 4: If I get diagnosed with a CI, it would be difficult to survive, so I do not need the payout.

Given the advancement in medicine, it has now become far easier and quicker to detect various illnesses. Early detection saves lives.

While cancer incidence rates in Singapore have risen over the years, mortality rates have declined due to improvements in survival rates. From 2017 to 2021, there were 42,876 cancer cases in females in Singapore, out of which, there were 13,419 cancer deaths. This translates to an average survival rate of over 67%, and the number could be higher for those who detected their cancer in the early stages.

Additionally, the age-standardised mortality rate for stroke in Singapore is 13.9% in 2021, and the number of deaths due to stroke within 30 days from the onset of stroke stands at a mere 7.5%. The chances of survival are much higher for those who are younger, with a mortality rate of just 0.1% for those 15-29, 0.9% for 30-39, and 3.7% for 40-49.

The lump sum payout from a CI plan can help you get your life back on track after the treatment, ensuring that you have a better quality of life, and giving you time to recuperate before returning to the workforce.

Myth 5: I am still young so I don’t need CI insurance yet

While it is true that the occurrence of CI in the elderly is more frequent than among young adults, younger individuals are not completely immune from illness.

From 2017 to 2021, there were 42,876 cancer cases in females in Singapore, and 41% of those diagnosed were under 60 years old. In 2021, there were 196 individuals diagnosed with stroke among the 15 to 39 age group, and 578 in the 40 to 49 group.

Furthermore, by waiting to get CI insurance at an older age, there is a risk of developing a medical condition that can cause you to be excluded from certain coverage.

In conclusion…

According to the 2022 Protection Gap Study, an average working adult in Singapore requires a CI coverage that is approximately 3.9 times their annual income.

However, most are grossly under-protected. This is despite CI plans costing as little as S$9.15 a month.

With medical advancements, mortality rates for CI are now lower and having a CI plan can help facilitate better care during the recovery period. Plan ahead so you are covered for life’s unexpected curveballs. Come talk to us at ask@plannerbee.co and let us help you today.

Read more: Best Critical Illness Insurance