What is Buy Now Pay Later?

Buy Now Pay Later (BNPL) allows you to divide your purchases into smaller instalments, often without interest, instead of paying the full amount at once.

The idea of paying in instalments is not new, but BNPL apps have made the process quicker, simpler, and easier to access. In most cases, there are no credit checks involved.

Popular BNPL providers

Atome

Launched in 2019, Atome is one of the best-known BNPL providers in Southeast Asia. It is available both online and in stores, with partner brands including Sephora, Dyson, and Tangs.

For in-store shopping, you can scan and pay using a QR code on your mobile phone. Atome also offers online shopping vouchers, including S$10 off the first online purchase for new users.

Payments are automatically deducted from your chosen credit or debit card, so it is important to have enough funds in your account before the due date. If you miss a payment, the late fee is S$15 for orders below S$1,000 and S$30 for orders above that amount.

Grab PayLater

Grab PayLater can be activated directly within the Grab app and lets you spread payments over four monthly instalments, which is slightly longer than the three-month plans many other providers offer. You can use it when shopping online with brands such as Hipvan, Asus, and for groceries on GrabMart.

The service is only available for online purchases. Late payments incur a fee of S$15.

You can choose between PayLater Instalments or PayLater Postpaid. Instalments allow you to split each purchase, while Postpaid consolidates all your monthly spending into a single bill. Both options earn GrabRewards points, although the rate may differ depending on the merchant or payment method.

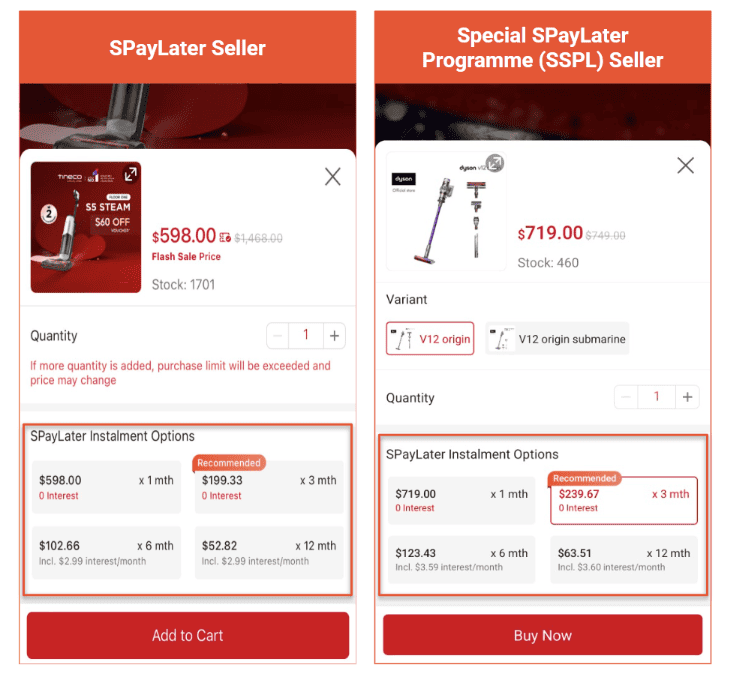

SeaMoney (SPayLater)

SPayLater is integrated within Shopee and available to eligible users at checkout. It allows you to pay in monthly instalments or defer your payment by one month.

The service is limited to Shopee and cannot be used on other platforms. If you miss a payment, a late fee of S$5 per order applies, and your account may be suspended until the outstanding amount is cleared.

Abnk.ai

Abnk.ai is one of the newer BNPL providers in Singapore, offering an AI-driven payment solution. It allows customers to pay in instalments both online and in stores with various partner brands.

Late fees are charged at a fixed rate based on the outstanding balance and how long the payment is overdue. The service integrates easily with e-commerce platforms and can be accessed through its mobile app.

Comparison of popular BNPL providers in Singapore

| Provider | Key features | Late payment fees | Availability |

| Atome | Online and in-store with brands such as Sephora and Dyson | S$15 (below S$1,000), S$30 (above S$1,000) | iOS, Android |

| Grab PayLater | Four-month instalments for online shopping | S$15 per missed payment | |

| SeaMoney (SPayLater) | Shopee-only purchases, instalments or deferred payment | Up to S$5 per order; account may be suspended | |

| Abnk.ai | AI-driven, flexible for online and in-store purchases | Fixed fee based on balance and duration of delay |

Pros and cons of using BNPL services

Buy Now, Pay Later (BNPL) can be convenient, but it also carries risks if not managed well. Here is what you should know.

Pros

1. Immediate access to purchases

BNPL allows you to buy something straight away, even if you cannot pay the full amount at once.

2. Interest-free instalments without extra charges

Unlike credit card instalment plans, BNPL does not usually include processing fees. You can also repay early without facing the high early repayment charges that credit cards often apply.

Cons

1. Late payment fees

BNPL providers earn revenue from late payment charges. These may look small at first, but they can add up over time and cause debt if you are not careful.

2. Fixed repayments dues

BNPL does not allow you to choose or postpone your repayment dates. Payments must be made on the set schedule.

BNPL vs Credit card instalments

Credit card instalment plans often include a one-off processing fee, usually between 3% and 6% of the purchase amount, and may apply early repayment or cancellation charges. On the positive side, these instalments count towards your monthly card spend and can sometimes earn rewards, depending on your bank.

BNPL usually costs less as it avoids processing and early repayment fees, making it cheaper for short-term purchases. However, you must follow the payment schedule strictly. Payments cannot be delayed, and missing a due date results in a late fee and suspension of your account until the payment is cleared.

Read more: Zero-based Budgeting 101: How to Use it to Maximise Your Finances and Achieve Your Money Goals

Use BNPL responsibly

Plan your purchases

Check your existing financial commitments before using BNPL. Make sure you will have enough funds to cover future payments so that you do not fall into debt.

Set a reminder before payment due date

Mark payment deadlines in your calendar to avoid late fees. Remember that BNPL is essentially borrowing against your future income. Be cautious not to overcommit, as unexpected expenses can still arise.

Read more: What Drives Impulse Spending and How To Avoid It

A word of caution

BNPL can make purchases look more affordable by splitting them into instalments, but it is still a form of debt. Because most providers do not carry out strict credit checks, it is easy to overspend or sign up for multiple plans without realising how much you owe in total. Small payments may appear manageable on their own, but they can quickly add up alongside other financial commitments.

Missing a payment leads to late fees, and your account may be suspended until the balance is cleared. If late payments continue, your credit score could also be affected, which may limit your ability to borrow in the future. To avoid these risks, treat BNPL carefully, keep track of all instalments, and avoid using it for everyday spending.

Read more: Understanding Lifestyle Creep and How To Break Free