An Integrated Shield Plan (IP) is one of the most popular health insurance options that helps cover hospitalisation costs. Different plans offer varying levels of coverage. Some provide coverage for higher-class wards, like Class A or B1 in public hospitals, while others extend to private hospital stays.

An Integrated Shield Plan combines MediShield Life with private health insurance for extra coverage. You can also add a rider to reduce or fully cover deductibles and co-insurance.

Since IPs generally provide similar coverage, you can only have one at a time through MediSave. Medical bills can only be claimed from one plan, so it’s important to choose the right one for your needs.

Should you upgrade to an IP?

MediShield Life covers all Singaporeans and Permanent Residents (PRs) for life, regardless of age or pre-existing health conditions. You might wonder if you still need an IP.

Here are some key points to consider:

- Hospitalisation comfort: MediShield Life is designed for subsidised treatment in public hospital Class B2 and C wards. If you prefer staying in a private hospital or a higher-class ward (Class A or B1) in a public hospital, you will need an IP for coverage.

- Budget and affordability: IP premiums increase with age. Consider whether you can afford these costs in the long run.

- Additional coverage: Private insurers offer riders to cover co-insurance and deductibles under MediShield Life. These riders require separate premiums, which must be paid in cash and cannot be deducted from MediSave.

Read more: Debunking Myths About Integrated Shield Plans

How to check if you have an IP?

If you’re uncertain of whether your current health insurance plan is an Integrated Shield Plan, you can simply log on to the Central Provident Fund (CPF) website to check. Make sure you have your SingPass in order to check.

- Go to gov.sg

- Log on to my CPF Online Services

- Go to “My Messages“

- See “Insurance” section

What does an IP cover?

The benefits of standard Integrated Shield Plans (IPs) are generally similar across insurers, but they may offer different coverage for private hospitals and Class A plans.

In general, a standard IP covers the following:

1. Outpatient treatment for kidney and cancer treatments

This includes treatments like kidney dialysis, cancer therapies (such as chemotherapy and radiotherapy), stereotactic radiotherapy, and immunosuppressants for organ transplants.

2. Inpatient and day surgery

This covers treatment costs, daily ward fees, and surgery costs. Diagnostic endoscopies are also covered, even if they don’t lead to hospitalisation, as they are considered day surgeries. However, policy terms may vary, so check with your insurer for details.

A Class A IP may provide additional coverage, such as:

3. Selected pre- and post-hospital treatment

This includes outpatient care before and after hospitalisation, such as follow-up consultations or treatments. These must be managed by the same doctor who oversaw the hospital admission.

4. Serious complications from pregnancy and delivery

Not all pregnancy-related costs are covered, but certain serious complications can be claimed. This may include treatments for congenital anomalies or complications like miscarriage after 13 weeks of pregnancy or ectopic pregnancy. Coverage varies by insurer, so it’s important to confirm with your provider.

What is not covered by an IP?

1. Outpatient diagnostic scans and scopes

Outpatient diagnostic procedures like MRI scans, CT scans, X-rays, and health screenings are typically not covered unless they lead to hospitalisation, inpatient treatment, or form part of pre- or post-hospitalisation care.

2. Regular pregnancy delivery

Normal deliveries without complications are not covered. However, you can use your MediSave Maternity Package for pregnancy-related costs, including ultrasounds and consultations.

3. Non-medically necessary treatments

Cosmetic treatments and procedures that are not medically necessary are excluded.

4. Pre-existing conditions

Conditions that existed before you took out the policy are generally not covered, unless specified otherwise in the policy.

5. General exclusions

In general, non-medically necessary treatments, such as fertility treatments or cosmetic surgery, are typically excluded.

It’s crucial to review your policy carefully to understand the coverage and exclusions, as these can vary depending on the insurer and plan type.

In a nutshell, an IP:

| Provides coverage for | Does not provide coverage for |

|

|

Which insurers offer IP?

At the moment, there are seven private insurers offering IPs. These include:

- AIA Singapore Private Limited’s HealthShield Gold

- Great Eastern Life Assurance Co’s SupremeHealth

- HSBC Life (Singapore) Private Limited’s HSBC Life Shield (Previously by AXA Life)

- Income Insurance Limited’s IncomeShield and Enhanced IncomeShield

- Prudential Assurance Company Singapore’s PRUShield

- Raffles Health Insurance’s Raffles Shield

- Singapore Life Limited’s Singlife Shield (Previously Myshield by Aviva)

Find out more about the best integrated shield plans here.

How do I pay for my IP premiums?

You can pay your IP annual premiums using MediSave, just like with MediShield Life. However, be aware that there is a limit on the amount of MediSave that Singapore residents can use for their IP premiums.

The amount that can be offset from their MediSave to pay for their IP premium is called the Additional Withdrawal Limit. The limits are as follows:

| Age group | Additional Withdrawal Limits |

| 40 & below | S$300 |

| 41 – 70 | S$600 |

| 71 & above | S$900 |

However, premiums for riders attached to your IP cannot be paid using MediSave and must be settled in cash.

Understand the claims process

IPs work on a reimbursement basis, so you usually pay for your medical expenses upfront and then submit a claim to get the money back. However, there are ways to reduce the need for large initial payments. Your claim limits will depend on whether you have a rider and if your treatment is provided by an insurer-approved doctor.

According to the Ministry of Health, most insurers typically take between one to four days to process claims.

To ensure a smooth claims process, make sure your claim meets these criteria:

- The claim amount is above the deductible

- The medical condition is covered by your policy

- It does not fall under general exclusions, such as pregnancy and maternity expenses

Pre-authorisation for scheduled treatments

For scheduled treatments, some IP insurers offer pre-authorisation. This helps you understand your coverage beforehand, so you can make more informed healthcare decisions and feel more at ease.

With pre-authorisation, you can also enjoy cashless admission. The bill is sent directly to your insurer, reducing or removing the need for upfront payments. Plus, it may increase your claim limits, offering extended coverage for pre- and post-hospitalisation treatments and higher overall claim limits.

Letter of Guarantee (LOG) – available only for Singaporeans and PRs

If your hospital can obtain a Letter of Guarantee (LOG) from your insurer during hospitalisation, it may reduce or even waive the upfront cash deposit. An LOG is a letter from your insurer to selected hospitals, covering part or all of the deposit, depending on the estimated insurance coverage.

This is an additional service offered by insurers. All inpatient insurers provide LOGs, so it’s worth checking with your insurer for more details. After your discharge, you may still need to settle the hospital bill while your insurer processes the claim. Once the insurer settles the payment, any excess amount you’ve paid will be reimbursed accordingly.

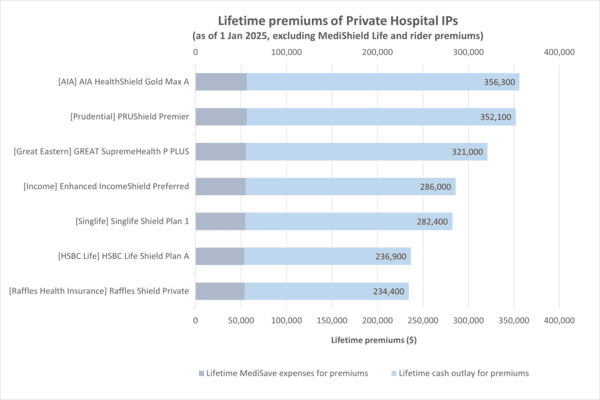

Can you afford the long-term cost of IP premiums?

The affordability of an IP depends on factors like age, type of coverage, and the insurer. Premiums tend to increase with age. While basic plans may have manageable premiums, additional coverage (e.g., for private hospitals) or including riders can raise the cost. To assess affordability, compare the total premium costs over time and consider your budget in the years ahead.

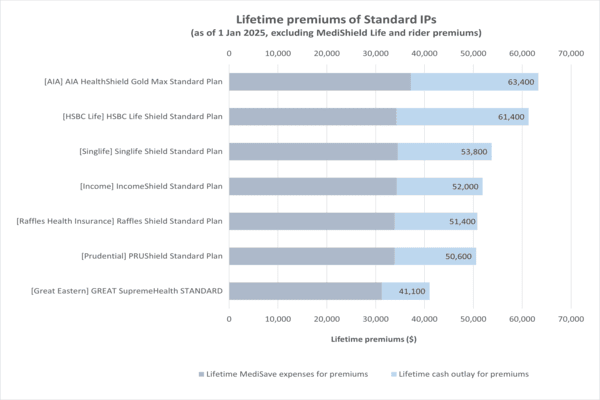

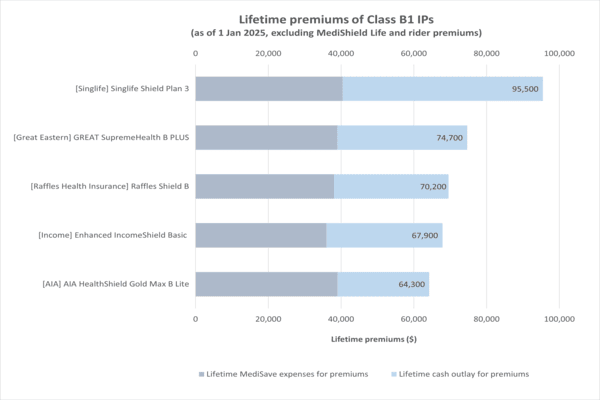

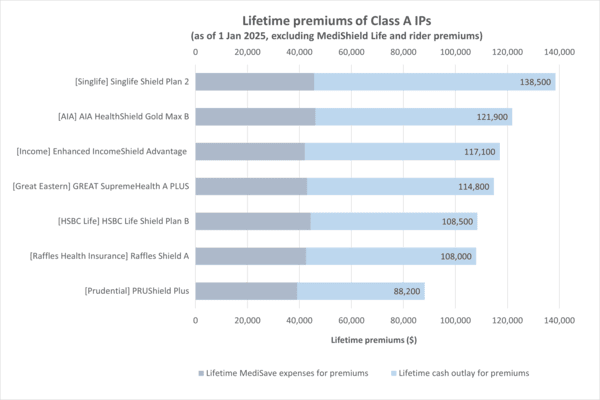

Here’s an illustration of lifetime premiums across various IPs, courtesy of the Ministry of Health.

Standard IPs

Class B1 IPs

Class A IPs

Private hospital IPs

Lifetime premiums are calculated by summing premiums from age one to 100, based on insurers’ rates as of January 2025. This does not include MediShield Life or rider premiums. Figures are rounded to the nearest hundred and are provided for general information only. Actual premiums may vary as insurers update their rates periodically.

Do you have enough health coverage?

When buying an Integrated Shield Plan, it’s important to consider your needs, comfort levels, and budget.

Compare the Integrated Shield Plans available and find one that best fits your needs. To make the decision easier, get a free, personalised quotation with a customised breakdown of your options, helping you choose with confidence. You can also refer to the MOH comparison for additional insights and a broader market view.

Still unsure or need more guidance? Drop us an email at ask@plannerbee.co—we’re happy to help!